Market Commentary

June opened with lingering tightness carried over from the May DOT Blitz and Memorial Day crunch. Most lanes are finding their footing, but California is in full seasonal peak and long-haul rates aren't backing down.

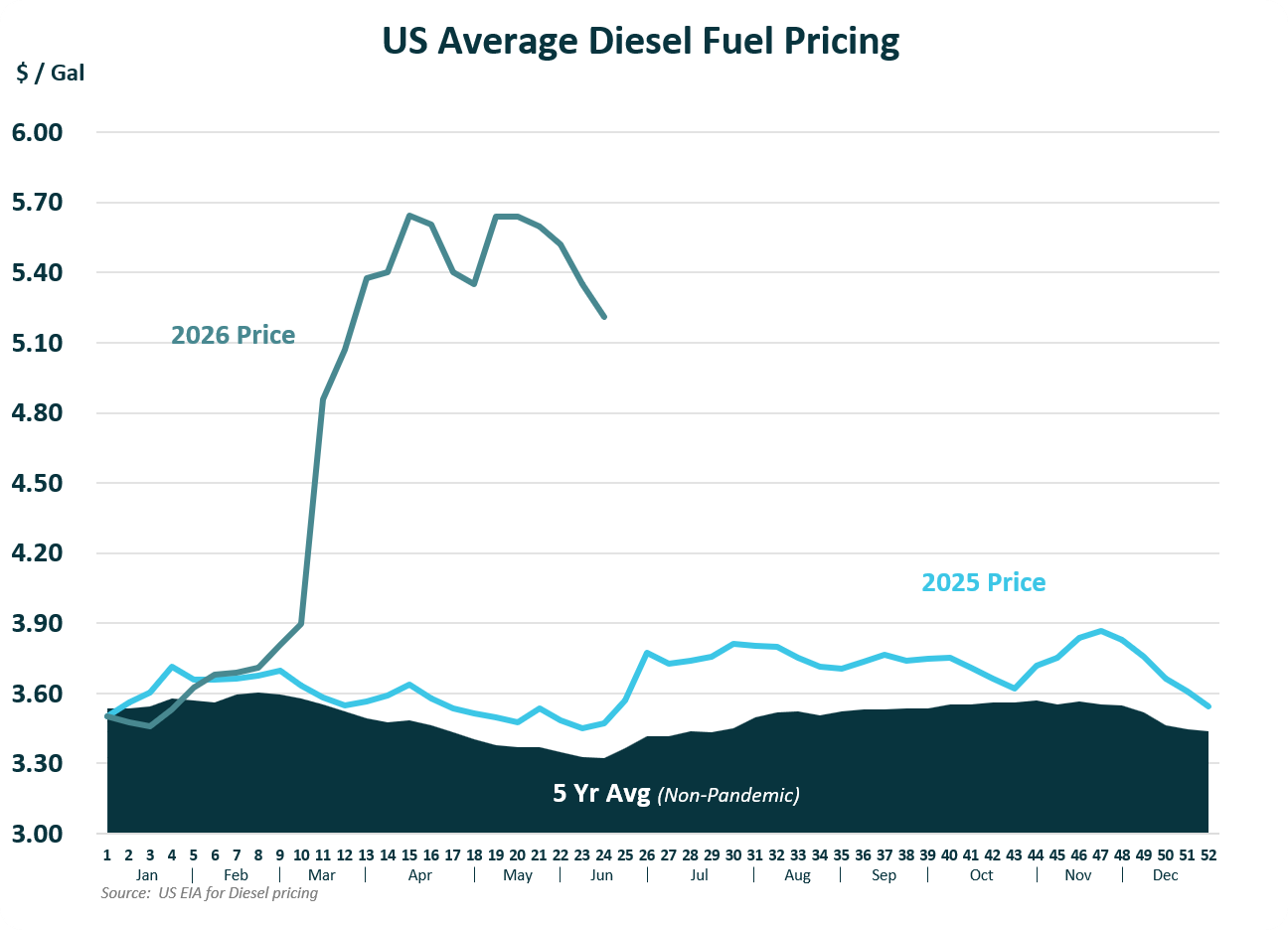

Diesel is pulling back from 2026 highs, though slowly. Expect modest normalization through mid-June outside of seasonal corridors, with July picking back up on produce-driven demand.

Market Commentary

The first week of June carried the weight of May. The DOT Blitz pulled capacity off the road, Memorial Day stacked volume behind it, and most lanes are now stabilizing.

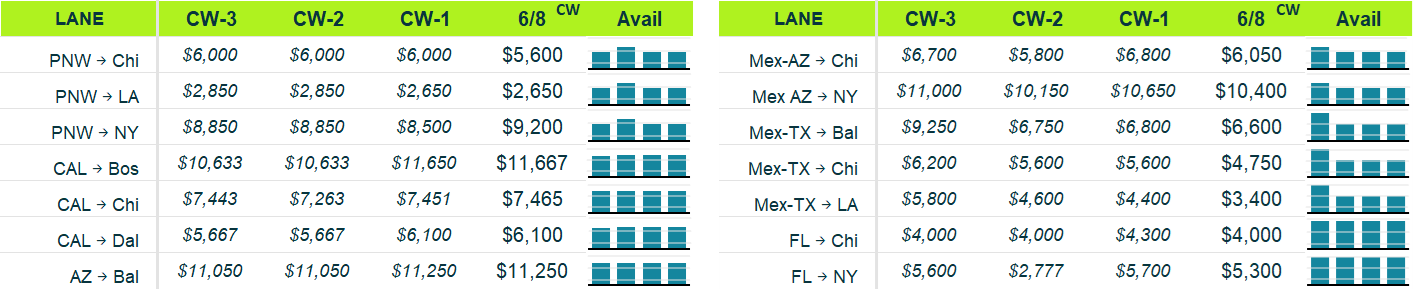

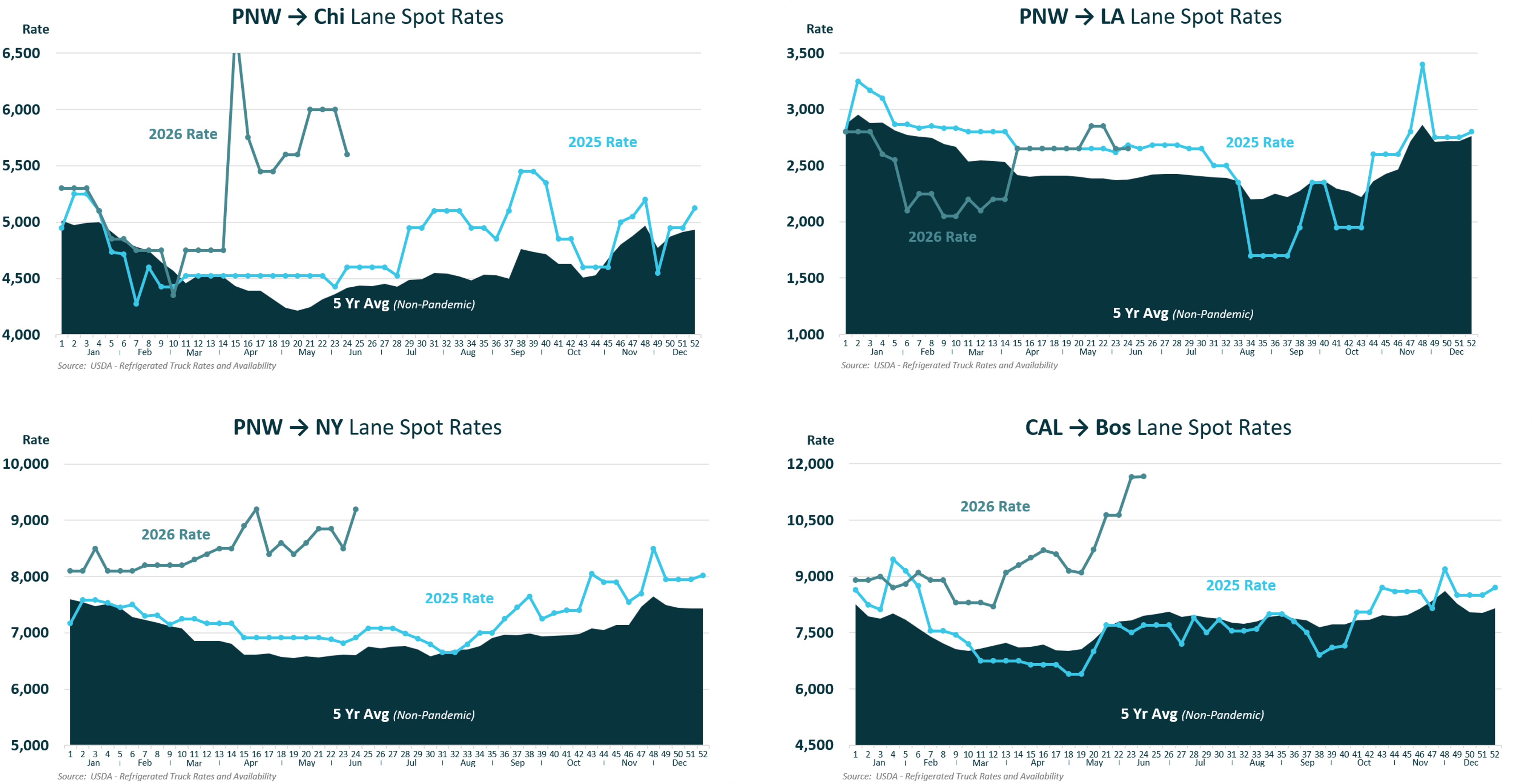

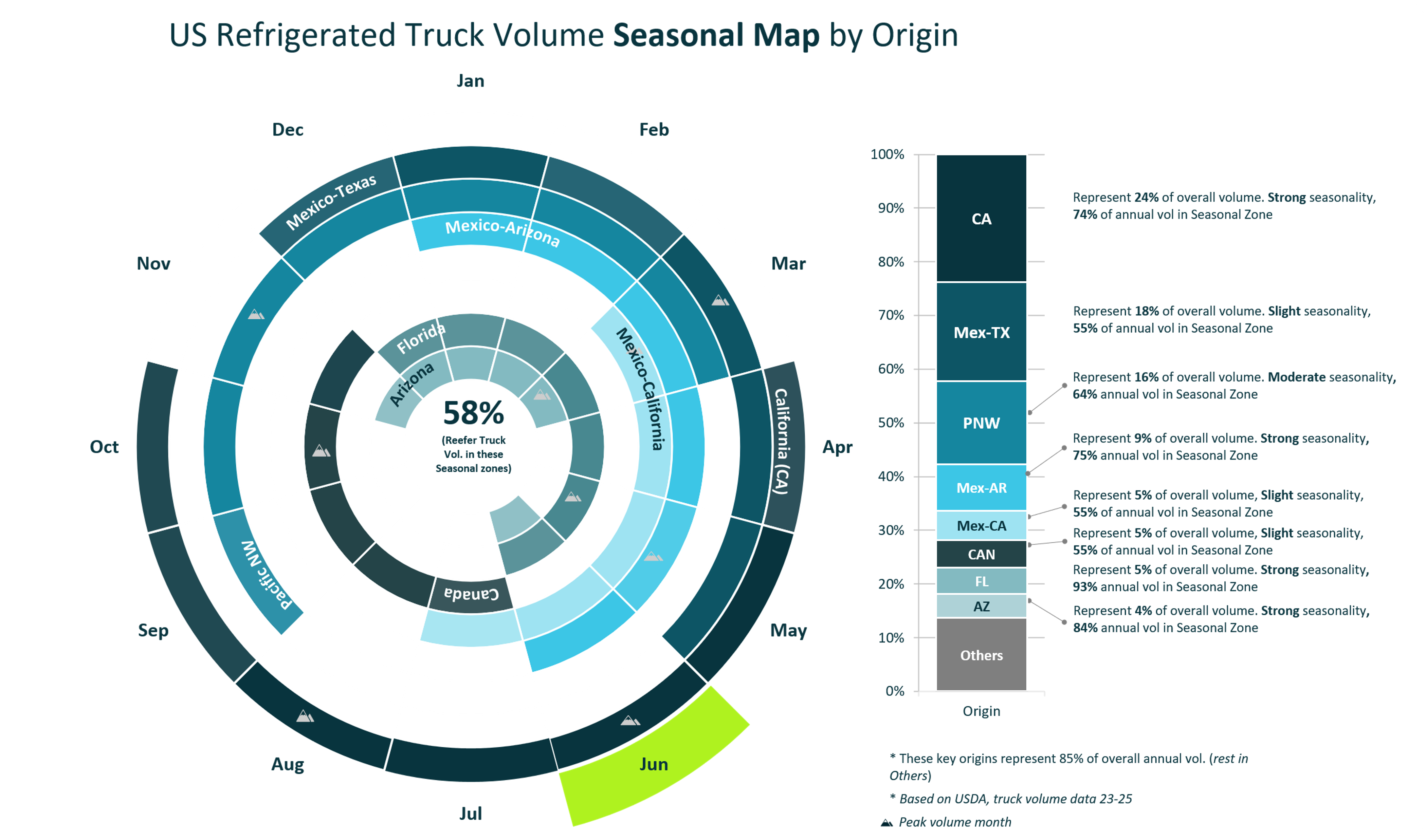

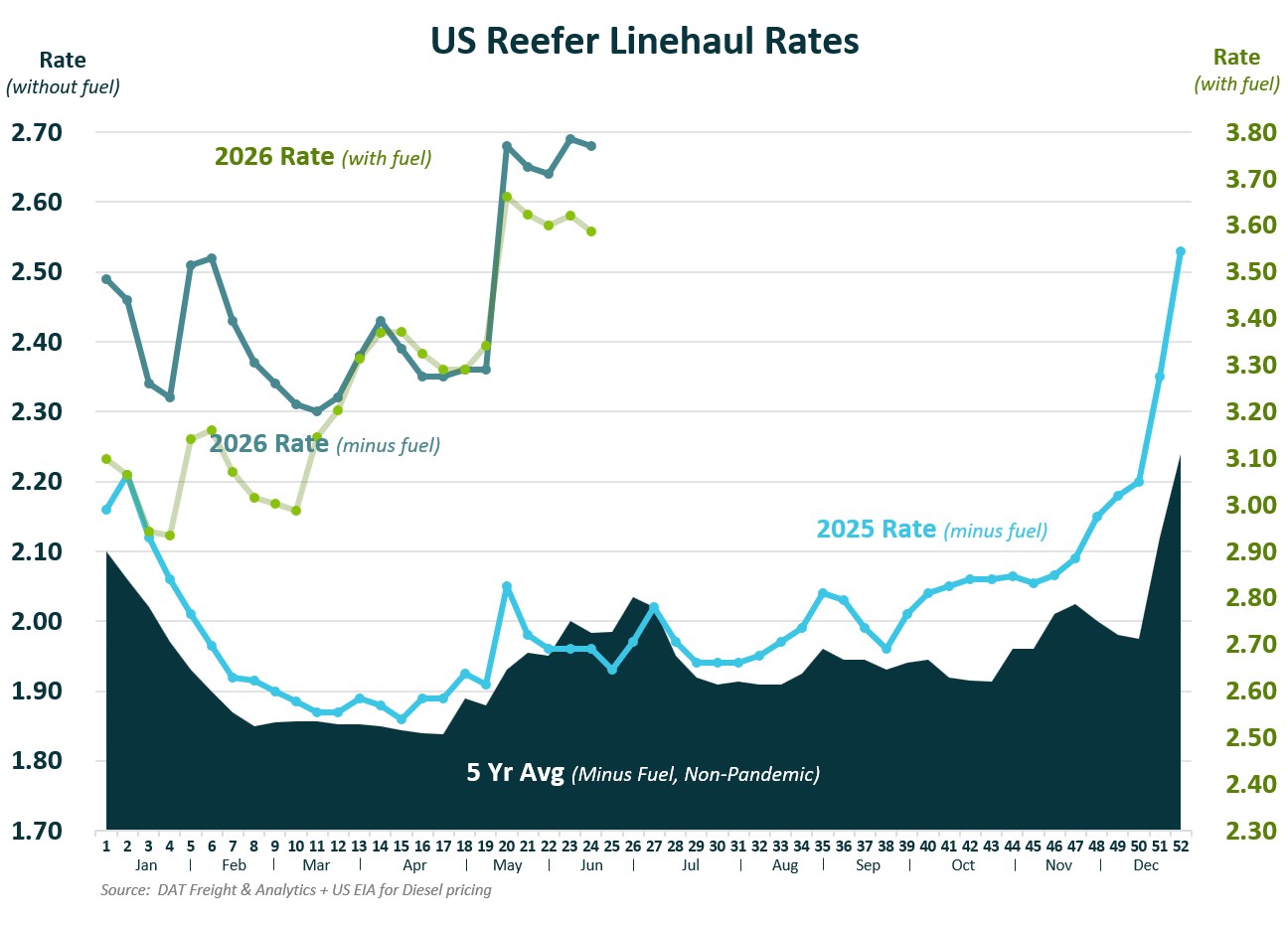

California is the clear exception. The seasonal map shows CA representing 24% of overall reefer volume, with 74% of its annual volume concentrated in the seasonal zone, which peaks in June. Rates on CAL to Boston are sitting above $11,600. That's not softening anytime soon.

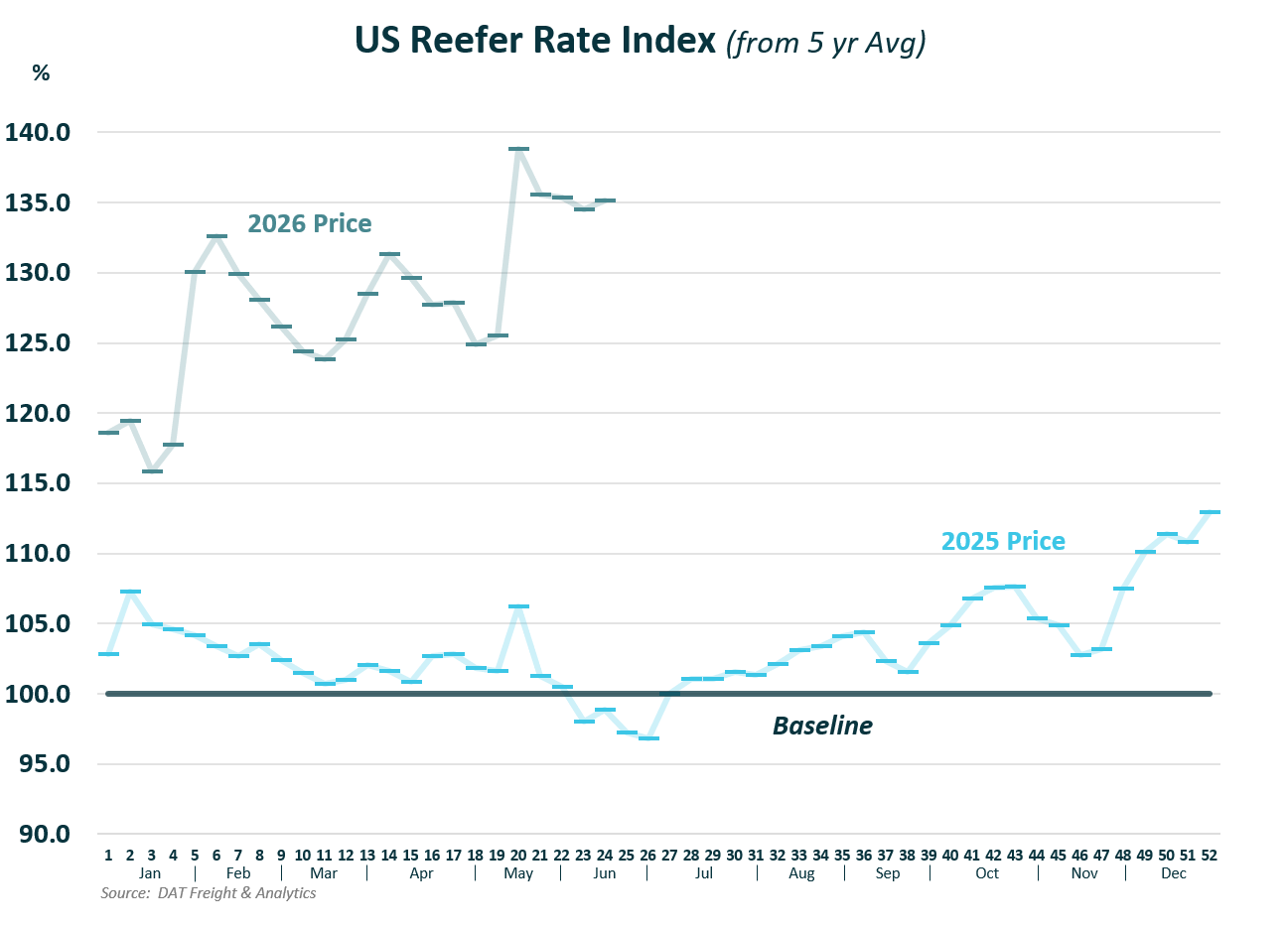

The reefer rate index is tracking notably above the 5-year baseline, though it's off its spring peak. Diesel pricing has come down from 2026 highs but remains well above the non-pandemic average, which is why carriers aren't passing savings through yet.

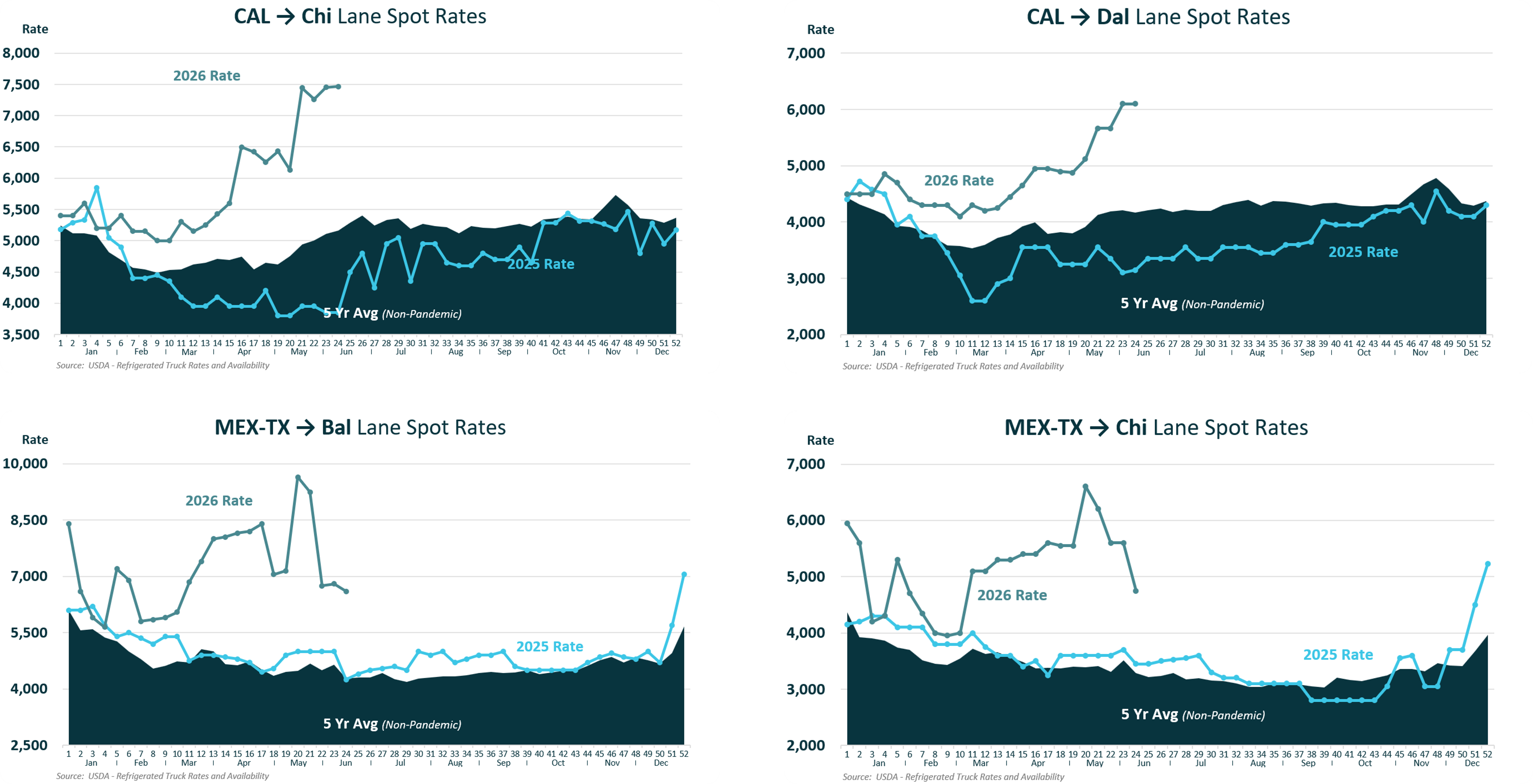

Mexico-Arizona to Chicago is running around $6,050 with tight availability. These Southwest origin lanes are in their peak window and capacity is competing with California volume at the same time.

Plan July capacity now on California and Southwest lanes. Waiting will cost more than acting early. Read more here on how to prepare for volatility

Lane Rate Progression